For federal employees, the Thrift Savings Plan (TSP) is one of the most powerful tools for building a secure financial future. Becoming a TSP millionaire is a goal that many strive for, and while the concept is simple, the journey is not easy. It involves consistent contributions, the discipline to stay the course during market fluctuations, and a commitment to long-term financial planning.

This article explores how small contributions over time can grow into a substantial nest egg through the power of compounding interest and the challenges that federal employees face in achieving this goal.

The Power of Compounding Interest

Compounding interest is the process where the earnings on your investments generate their own earnings. Over time, this snowball effect can lead to exponential growth of your retirement savings. The earlier you start contributing to your TSP, the more you can take advantage of compounding.

An Example of Compounding

Let’s say you start with a TSP balance of $0 and contribute $500 per month. Assuming an average annual return of 7%, here’s how your investment can grow over time:

- 10 years: $83,859

- 20 years: $247,924

- 30 years: $574,461

- 40 years: $1,248,116

By contributing regularly and allowing your investments to grow over time, you can see how the power of compounding can turn modest contributions into a substantial amount.

Consistent Contributions: The Key to Success

One of the biggest challenges in becoming a TSP millionaire is maintaining consistent contributions. Life’s financial demands can make it tempting to reduce or pause your contributions. However, even small, regular contributions can make a significant difference over the long term.

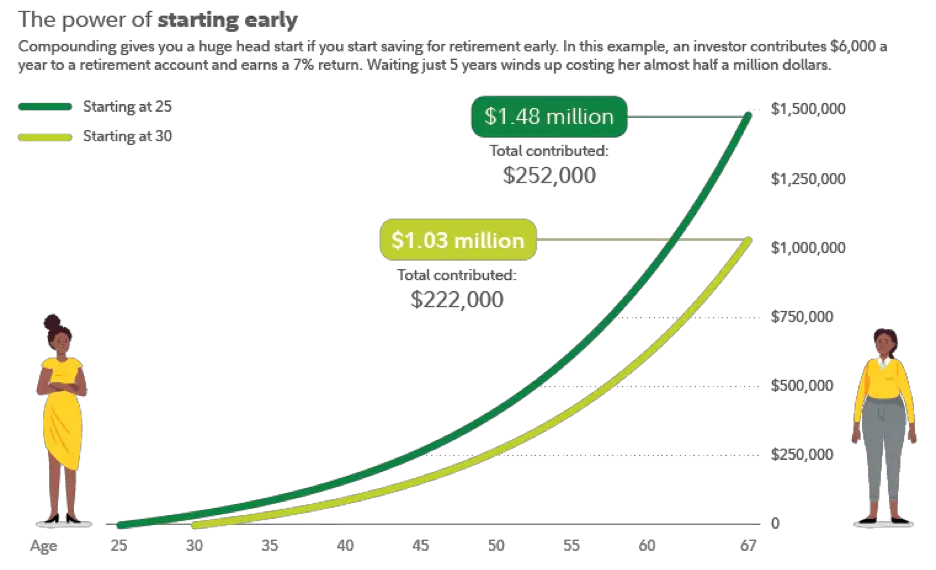

Starting Early

The earlier you start contributing, the more you benefit from compounding interest. Young federal employees should prioritize starting their TSP contributions as soon as possible, even if it means contributing a smaller amount initially. Over time, these contributions can add up significantly.

Look at the image below. Starting contributions just 5 years early can equate to nearly half a million dollars in additional money at retirement. Even though you only contributed an additional $30k over that time.

That’s the true power of compounding interest.

Increasing Contributions

As your salary increases over the years, consider increasing your TSP contributions. The TSP allows for automatic increases, which can be a great way to ensure you are consistently saving more as your income grows. The goal is to eventually max out your contributions to take full advantage of the tax benefits and employer matching.

The Importance of Staying the Course

Market volatility is a reality that every investor must face. The temptation to move your investments in response to market downturns can be strong, but this often leads to poor investment decisions and reduced returns.

Avoiding Emotional Decisions

When the market takes a dip, it can be tempting to move your investments to safer options. However, this often means selling low and buying high, which is the opposite of a successful investment strategy. Instead, stay the course and remember that the market has historically recovered from downturns.

Rebalancing Your Portfolio

Periodic rebalancing of your TSP portfolio can help ensure that your asset allocation remains aligned with your risk tolerance and retirement goals. This involves selling portions of your investments that have performed well and buying more of those that have underperformed to maintain your desired allocation.

The Impact of Fees

One advantage of the TSP is its low fees compared to many other retirement plans. Lower fees mean that more of your money stays invested, allowing compounding to work more effectively. Be mindful of the impact of fees on your investments and try to minimize them wherever possible.

The Role of Diversification

Diversification is a key principle in managing investment risk. The TSP offers a range of investment options. Each of these funds has different risk and return characteristics, allowing you to create a diversified portfolio that suits your risk tolerance.

Allocating Your Investments

A well-diversified portfolio seeks to manage risk and improve returns over time.

A common mistake is to be too conservative, too early in your career. In order to become a TSP millionaire, you’ll need to take some risk in the market. Just remember, that there’s no free lunch. The price you pay for a higher rate of growth over time is volatility, so you’ll need to be okay with some fluctuation in your account.

The Importance of Financial Education

Understanding the basics of investing and the TSP can significantly enhance your ability to make informed decisions. Many federal employees are not fully aware of the benefits and options available through the TSP. Taking the time to educate yourself can pay off substantially in the long run.

Resources for Federal Employees

The TSP website offers a wealth of information, including calculators, webinars, and articles to help you understand your options and make informed decisions. Additionally, consider consulting with a financial advisor who specializes in serving federal employees to get personalized advice.

Overcoming Common Challenges

While the principles of becoming a TSP millionaire are straightforward, several common challenges can derail your efforts:

Prioritizing Saving Early On

Many young employees prioritize other financial goals, such as buying a home or paying off student loans, over saving for retirement. While these are important, it’s crucial to find a balance that allows you to start saving for retirement as early as possible.

Staying Invested During Market Pullbacks

The emotional impact of market downturns can lead to panic selling. Maintaining a long-term perspective and understanding that volatility is a normal part of investing can help you stay invested and benefit from eventual market recoveries.

Balancing Other Financial Goals

Life events such as marriage, children, and education expenses can impact your ability to contribute to your TSP. Developing a comprehensive financial plan that includes all your financial goals can help you stay on track with your retirement savings.

Conclusion

Becoming a TSP millionaire is simple in theory but challenging in practice.

It requires consistent contributions, staying the course during market fluctuations, understanding the impact of fees, and maintaining a diversified portfolio. By starting early, increasing contributions over time, and avoiding emotional investment decisions, federal employees can leverage the power of compounding interest to build substantial retirement savings.

Educating yourself and seeking professional advice can further enhance your ability to reach this significant financial milestone.

Remember, the journey to becoming a TSP millionaire is a marathon, not a sprint, but with discipline and perseverance, it can be achievable.

Austin Costello is a Financial Advisor who helps educate federal employees on what it takes to achieve retirement and reduce financial stress. He and his firm, Capital Financial Planners, host educational webinars at various government agencies and work with hundreds of individual clients.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. Investing involves risk including loss of principal. No strategy assures success or protects against loss.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

This is a hypothetical example and is not representative of any specific situation. Your results will vary. The hypothetical rates of return used do not reflect the deduction of fees and charges inherent to investing.